We use cookies on our website to personalize your experience, analyze site usage, and improve our marketing efforts. By continuing, you agree to the terms of our Privacy Policy.

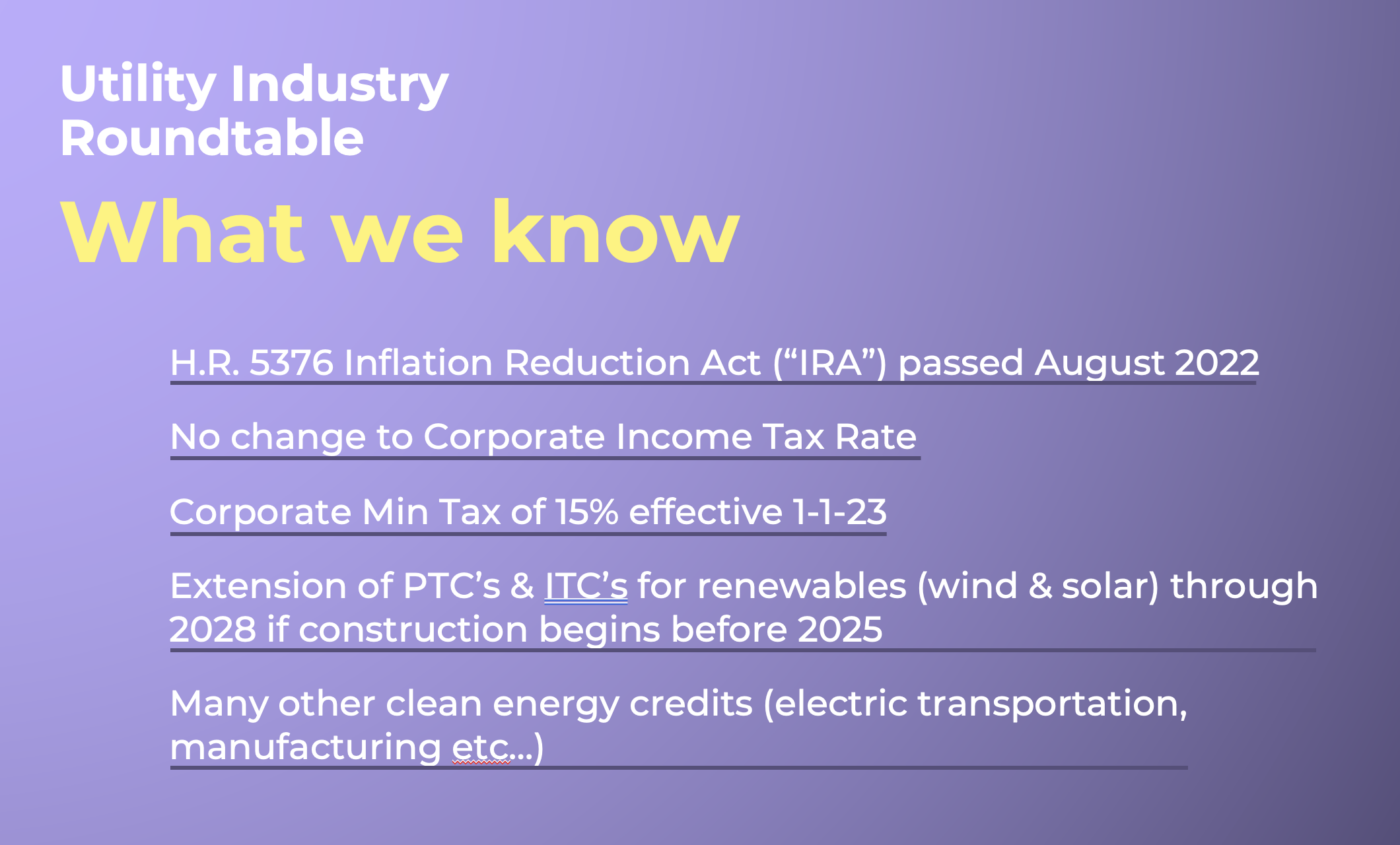

Considering the impact of the 2022 Inflation Reduction Act for Utility tax and regulatory

INDUSTRY UNCERTAINTY

H.R. 5376, known as the Inflation Reduction Act, introduces legislation that will affect our industry across many facets. From our conversations with utility leaders, we know there are ongoing questions:

How will we determine if we are an “Applicable Corporation” subject to the new corporate minimum tax?

What will make the definition of “Adjusted Financial Statement Income” (“AFSI”)?

How will my systems calculate and record two types of taxes?

What will I be able to recover from my customers from a regulatory perspective?

Are the normalization rules going to come into play?

What tools will I use to model the impacts on cash flows, earnings, and regulatory outcomes?

AUTOMATION POSSIBILITIES

A tailor-made, automated solution bringing sanity to complexity.

Learn how you can be confident and certain using innovative automation made possible with RCC’s Aggregate Singularity.

Rory Roberts of Entergy – determining what constitutes an Applicable Corporation

Matt Marcelia of Puget Sound Energy and Rory Roberts of Entergy – book depreciation expense addback challenges in determining Applicable Financial Statement Income

Rory Roberts of Entergy – determining rate base treatment for the min tax DTA and cost of service presentation early

Brad Coenen and Eric Nicolaus from Wisconsin Energy Group – strategic modeling including the multi-tiered and bonus credits for Renewable Energy

Jonathan Bass of Dominion Energy – Renewable Energy Tax Credits deep dive

In addition to other considerations and questions.